How Does it Work?

The program is a standard FHA Mortgage Loan (see

FHA Loans) that requires 3.5% Down Payment. That 3.5% required dowon payment is provided by the assistance program. Since FHA doesn't allow 100% financing, the assistance is provided as a second lien which is repayable each month. So essentially it's 100% financing.

Why is Our Program Different?

There are many Down Payment Assistance programs out there but our program differs in many ways.

Lower Credit Score While most Down Payment Assistance programs require minimum credit scores of 640-660, our program allows down to a 600 score. If you have a lower score due to past events, our program can help. Just need a good payment history for the last 12-24 months!

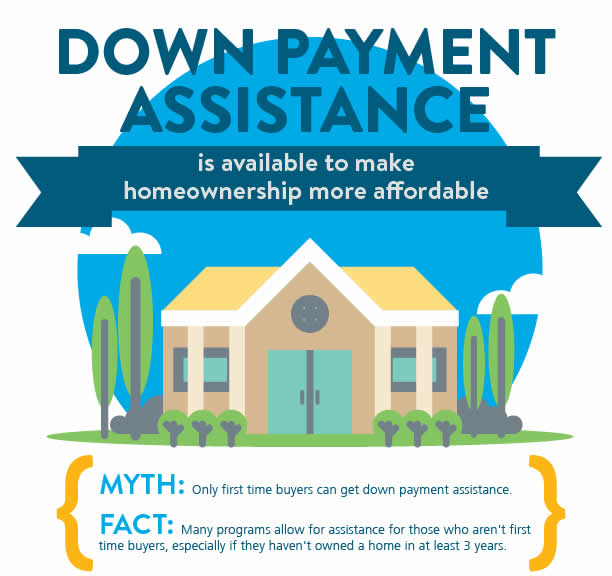

First-Time Homebuyer NOT Required Most Down Payment Assistance programs required all borrowers to be first-time homebuyers. Our program does not! We even allow you to use this program even if you currently own a home!

Income Limits Our program has NO Maximum Income Limit as most others do. The typically down payment assistance limit your household income to the Area Median Income or less in some cases. With our program, you can use even if your income is over the Area Median Income!

Purchase Price Limits Most other programs are targeting lower priced properties that are typically below the maximum limits set by FHA. Our program follows the FHA loan limits and even allow higher priced homes in high balance counties!

Pre-Payment Penalty Most other Down Payment Assistance programs have restrictions on refinancing the first mortgage. They do not allow within the first 3 years or have severe penalties if you do. Our program has no penalties to refinance when rates drop!

As you can see, our program has many benefits to buyers looking to purchase a home. We have helped thousands of clients on this program and you could be the next to become a homeowner!